Panama is one of the fastest growing economies in Latin America. Foreign investments in Panama amount to nearly 9 percent of the country’s GDP, which is the largest share in the Americas and speaks to the country’s investor friendliness.(1) Foreign direct investment into Panama is up 6 percent since 2013 and accounted for 11.3 percent of the country’s GDP in 2014.

With Panama boasting the second largest Free Trade Zone in the world, it’s easy to see why a thriving expat community (3,000 foreigners from 30 different countries) has stimulated the growth of new businesses owned by foreigners and locals alike. Investing in Panama is straightforward as the currency is in USD, there are no restrictions on foreign ownership, nor any exchange controls. The U.S.-Panama Trade Promotion Agreement from October 2012 granted U.S. exporters immediate duty free treatment accounting for more than half of current trade.(2) The country’s tropical climate is favorable to agricultural practices, and can permit up to two growing cycles per year with the proper farming techniques. Couple that with cool, mountain climate retreats, and Panama emerges as an ideal agricultural investment location with the added benefit of being a sought after retirement destination.

Panama’s particularly fertile soil and favorable growing climate afford the country many unique agricultural opportunities. The avocado, particularly the Panamanian Hass variety, is ideally suited for cultivation in Panama. In 2016, the United States purchased nearly 2.2 billion pounds of avocados, a 16 percent increase from the quantity sold in 2014. The U.S. organic avocado market grew by over 30 percent in volume in 2014 while still leaving plenty of room for growth in the market, both in the U.S. and abroad, as presently many smaller producers are unable to meet the growing demand and required consistency of destination markets. Given these conditions, an investment with a Panamanian organic avocado producer could yield an investor a 16-plus percent IRR over a 30-year period through a fully managed, turnkey investment of US$45,000 for 2.5 acres.

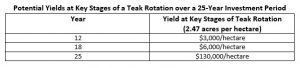

Forestry is also another potentially profitable opportunity in Panama, with over 50 percent of the country’s land being forested. As an example, teak has been valued for more than 2,000 years as a durable construction material and is now a worldwide coveted commodity. With the right management and timing, it’s possible to realize a yield of 10 percent IRR over a 20-plus year timeframe when investing in Panamanian teak. There are also reforestation visas available through the Panamanian government where investors can apply for a temporary Panamanian visa or permanent residency, depending on the type and amount of investment in addition to receiving a tax break on their Panamanian taxes. (3)

Mango cultivation in Panama also can be explored as a viable investment opportunity. With an average producing lifespan of 60-80 years depending on the variety, the mango is one of the more lucrative and dependable crops in the world. While the mango tree is native to Southeast Asia, the climate is quite similar in Panama and very conducive to mango production.

The United States is the greatest importer of mangos globally, accounting for a nearly 45 percent consumption rate of the world’s mango exports. Meanwhile, imports to European markets more than doubled between 1999 and 2008. Given Panama’s geographical proximity to both foreign markets and their strong business practices and incentives, exposure to the Panamanian mango export market could be a nice fit for a variety of investor classes. For example, an organic mango producer in Panama is projecting a nearly 17 percent IRR over a 30-year period for an initial investment of US$38,500.

The business and tax incentives in Panama are attractive to foreign investors. Panamanian income taxes (only 7 percent after the first US$9,000 and capped out at 27 percent) apply only to Panamanian-generated income. Capital gains taxes can be as low as 10 percent and all inheritance taxes have been completely abolished. The Foreign Investor Protection law grants foreign investors the same rights and freedoms as Panamanian citizens to own land.(4) There is also a law targeting reforestation investments that provides a 25-year income tax exemption to those who purchase farmland for the purpose of reforestation. Panama also boasts an all-around stable economy, where inflation is maintained at 2 percent with a Value Added Tax (VAT – similar to a U.S. sales tax) of zero. Property taxes are extremely affordable in Panama, with properties having a registered value of less than US$30,000 paying nothing and only 2.1 percent on properties more than US$75,000.(5) Investors in agricultural activities are exempt from paying Panamanian income taxes on their agriculturally-earned income if the annual income is under US$350,000 as well as taxes on income earned from exports. Agricultural investors are also exempt from Panamanian property taxes if their agricultural land is used exclusively for farming and the registered value of the property is less than $150,000. Exporters of non-traditional agricultural products (melons, watermelons, pumpkins, pineapples, etc.) enjoy the benefits of exemption from taxes for income earned from exports, duty-free importation of materials and equipment, and negotiable tax credits for amounts exported.(6) These foreign-friendly business practices, agricultural tax benefits, and extremely affordable tax rates make Panama an attractive agricultural investment opportunity worthy of further exploration.

[1] Alex, “Panama Farmland – A Guide to Agricultural Investment in Panama”, panama equity REAL ESTATE, September 2013, https://www.panamaequity.com/panama-farmland-a-guide-to-agriculture-investment-in-panama/, May 23, 2016.

[2] United States Department of Agriculture (USDA), “Panama”, USDA – Foreign Agricultural Services, n.d., http://www.fas.usda.gov/regions/panama, May 23, 2016.

[3] Jeff, “Panamanian residency visa investment through sustainable, environmentally friendly reforestation projects”, Panama Forestry, n.d., http://www.panamaforestry.com/, May 23, 2016.

[4] Michelle Martínellí and Rubén Irígoyen, “International tax – Panama Highlights 2015”, Deloitte Touche Tohmatsu Limited, 2015, https://www2.deloitte.com/content/dam/Deloitte/pa/Documents/tax/2015_PA_Tax-panamahighlights.pdf, May 24, 2016.

[5] International Living, “Taxes in Panama”, International Living Magazine, Agora Inc., 2013, https://internationalliving.com/countries/panama/taxes/, May 24, 2016.

[6] Alvaro Aguilar, “Panamanian Tax Exemptions”, International Law Office, January 28, 2005, http://www.internationallawoffice.com/Newsletters/Corporate-Tax/Panama/Fabrega-Molino-y-Mulino/Panamanian-Tax-Exemptions, May 24, 2016.